Should You Accept a Traumatic Brain Injury Settlement Offer?

In most cases, the answer is: not yet. A traumatic brain injury settlement is one of the most consequential financial decisions you will make, and it is permanent. Once you sign a release, you cannot reopen the case, even if your condition worsens or new symptoms appear years later. Before you accept, you need to understand what the offer actually covers, what it leaves out, and whether it accounts for the full trajectory of a brain injury that may affect you for decades.

At The Leiva Law Firm, we have handled serious traumatic brain injury cases in Northern Virginia, including a $4 million TBI settlement for a client struck in a T-bone collision at an intersection. That case was one of the top 10 personal injury settlements in Virginia for the year. Through that work and others like it, we have seen how insurance companies approach TBI claims and how much money is left on the table when injured people accept offers without fully understanding what they are giving up.

This article covers what to evaluate before accepting a TBI settlement, what a fair offer should include, and when it makes sense to keep negotiating.

Why Insurance Companies Offer Early TBI Settlements

Insurance companies are not on your side in this process. Their job is to close claims for as little money as possible. One of the most effective ways to do that is to make an early settlement offer before you know the full extent of your injuries.

The Brain Injury Association of America explains this directly: insurers offer settlements quickly because doing so limits the total amount they pay out on a claim. Early offers may look reasonable when you are focused on immediate medical bills, but they are calculated before anyone knows what your long-term care will cost.

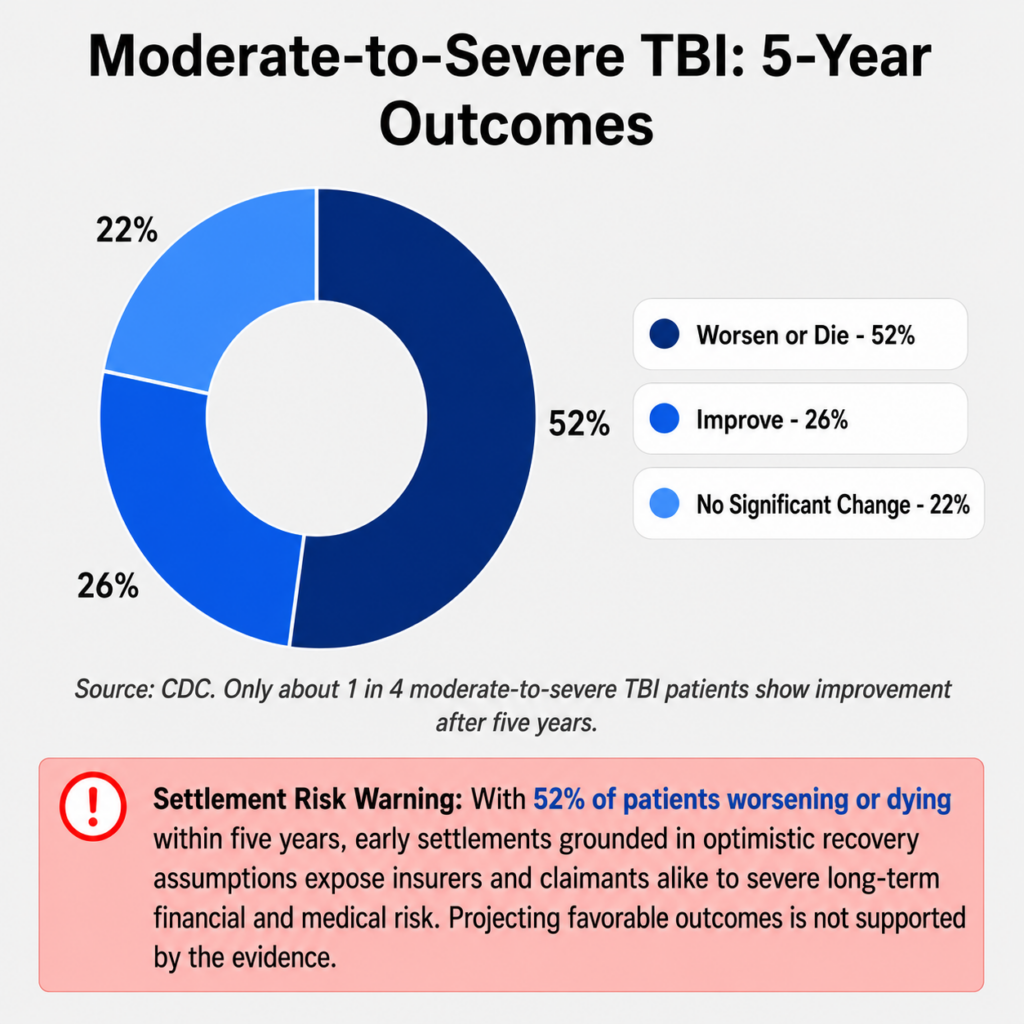

This matters because TBIs are unpredictable. CDC data show that only about 26% of moderate-to-severe TBI patients improve after five years, while roughly 52% worsen or die. An offer made in the first few months after your injury does not and cannot account for that trajectory.

What Can Go Wrong If You Settle Too Early

Three specific risks come with accepting a TBI settlement before you are ready.

Your Diagnosis May Not Be Complete

Brain injuries do not always show up on early imaging. Symptoms like memory loss, difficulty concentrating, personality changes, and emotional instability can emerge weeks or months after the initial injury. If you settle before reaching what doctors call maximum medical improvement (MMI), you may be giving up compensation for medical needs that have not yet surfaced.

First Offers Typically Undervalue TBI Claims

An insurer’s first offer is designed to test what you will accept, not to reflect what your case is worth. Their adjusters are focused on finding the lowest number you will take. If your injuries turn out to be more severe or longer-lasting than the initial offer assumed, you have no recourse.

You Permanently Waive Your Right to Future Compensation

This is the most important point. A settlement is a final agreement. You sign a release waiving all future claims related to this injury. If your condition deteriorates, if you need additional surgeries, if you can no longer work at the same capacity, none of that changes the deal you already signed.

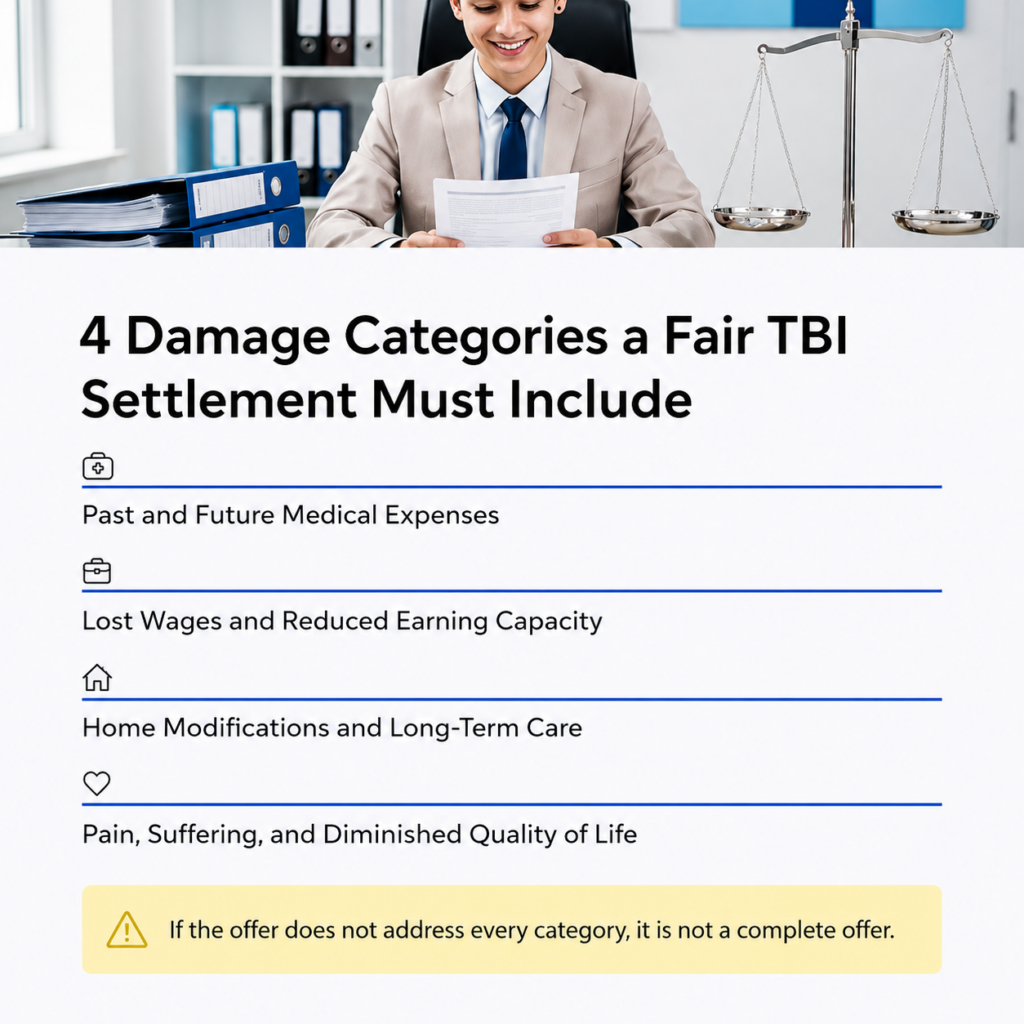

What a Fair TBI Settlement Should Cover

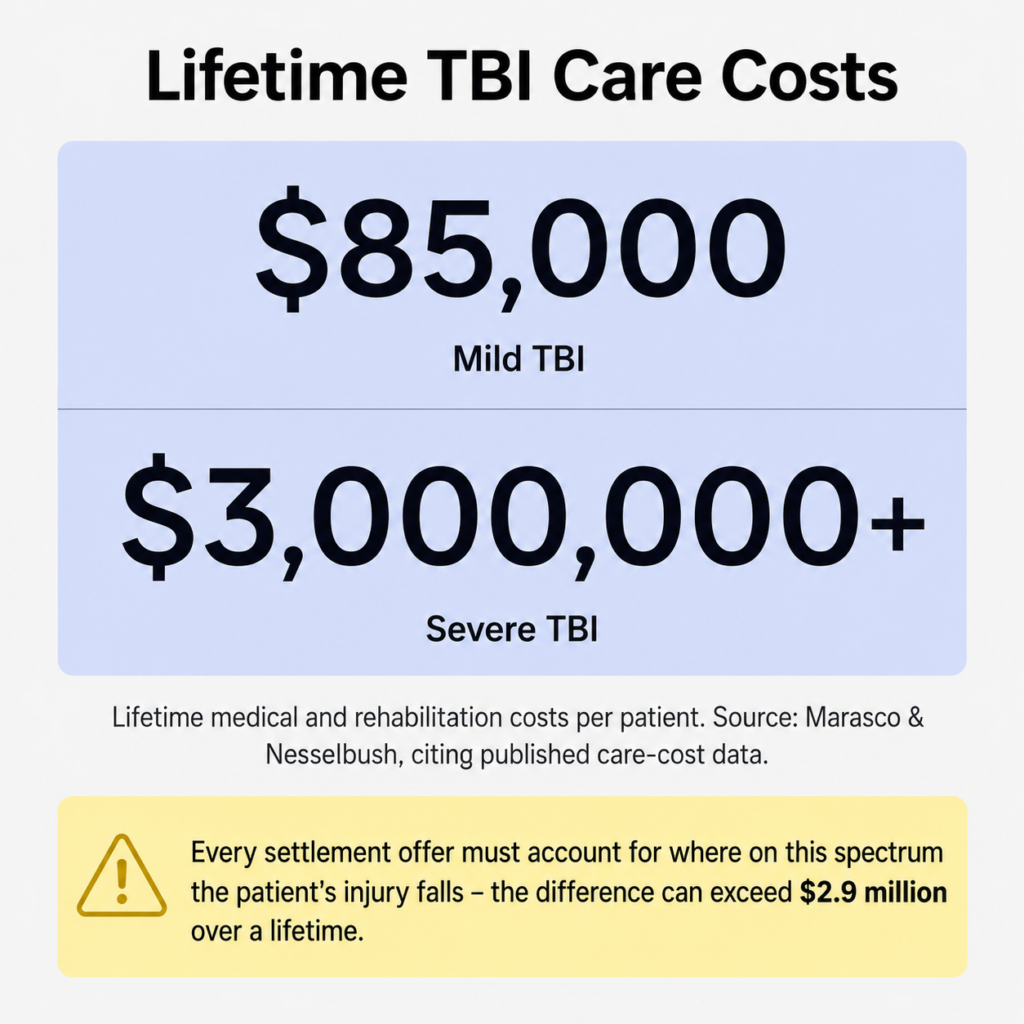

A TBI settlement that reflects the actual impact of your injury should account for far more than your current medical bills. Lifetime medical and rehabilitation costs for a single TBI patient can range from $85,000 to over $3 million, depending on severity. A moderate-to-severe TBI can cost $270,000 to $410,000 in the first year alone.

A fair offer should include all of the following categories:

- Past and future medical expenses. Hospital stays, surgeries, rehabilitation, physical therapy, occupational therapy, speech therapy, medications, and any ongoing medical monitoring.

- Lost wages and reduced earning capacity. Both the income you have already lost and the income you will lose in the future if the injury limits your ability to work at the same level.

- Home modifications and long-term care. If your injury requires in-home assistance, modifications to your living space, or full-time caregiving, those costs need to be in the number.

- Pain and suffering. The physical pain, emotional distress, and diminished quality of life caused by the injury. These are real damages, even though they do not come with a receipt.

If the settlement offer on the table does not address each of these categories, it is not a complete offer.

How to Evaluate a TBI Settlement Offer

If you have received an offer, there are concrete steps you can take to determine whether it is fair.

Wait Until You Reach Maximum Medical Improvement

MMI is the point at which your doctors determine that your condition is as stable as it is likely to get. Until you reach MMI, no one can accurately project your future medical needs. Settling before that point means guessing, and the insurance company is counting on your guess being lower than reality.

Add Up All Current and Projected Costs

Work with your medical team to estimate not just what treatment has cost so far, but what it will cost going forward. For serious brain injuries, this includes years or decades of follow-up care, therapy, and potential future surgeries.

Account for Lost Earning Capacity, Not Just Lost Wages

Lost wages cover the paychecks you have missed. Lost earning capacity covers the difference between what you could have earned over your career and what you can earn now, given your injury. For younger TBI patients or those in physically demanding jobs, this number can be substantial.

Compare the Offer Against Your Evidence

Accident reports, medical records, witness statements, and documentation of the other party’s negligence all factor into what your case is worth. The stronger your evidence, the more leverage you have.

Accept Now vs. Continue Negotiating

| Consideration | Accept the Current Offer | Continue Negotiating |

| When you receive money | Immediately (lump sum) | Longer timeline as negotiations or litigation proceed |

| Coverage of future costs | Fixed amount that may not cover long-term expenses | Potential for a higher amount that reflects actual projected costs |

| Future legal rights | Permanently waived. No additional claims possible | Preserved until you reach an agreement |

| Likely amount | First offers are typically below the full value of the claim | With strong evidence and representation, recoveries tend to be higher |

| Risk | Risk of accepting less than you need | Risk of a longer process, but with the potential for a fairer outcome |

How a Personal Injury Attorney Strengthens a TBI Claim

TBI cases involve complex medical evidence, long-term cost projections, and insurance companies with experienced adjusters working against you. An attorney who has handled catastrophic injury cases brings several things to the process that are difficult to replicate on your own.

Accurate Damage Calculation

Attorneys work with medical and economic experts to project your future care needs and earning losses. This is not guesswork. It is a structured analysis based on your specific diagnosis, treatment plan, and career trajectory.

Identification of All Liable Parties and Coverage

In a car accident case, for example, there may be multiple responsible parties, additional insurance policies (such as uninsured or underinsured motorist coverage), or product liability claims that increase the total available recovery.

Negotiation Leverage

Insurance companies evaluate claims partly based on the attorney on the other side. An attorney with trial experience and a track record in serious injury cases changes how the insurer approaches the negotiation. They know the case will go to trial if the offer is inadequate, and they adjust accordingly.

Contingency Fee Structure

Most personal injury attorneys, including our firm, work on contingency. You pay nothing upfront, and the attorney’s fee comes from the recovery. If there is no recovery, there is no fee. This means you can get qualified legal guidance without any financial risk.

Manuel Leiva’s background is relevant here. Before focusing on plaintiff-side personal injury work, he spent years at private litigation firms defending physicians in medical malpractice suits. He understands how the defense side evaluates claims, what arguments they will make, and where their strategies are vulnerable. That perspective, combined with over 25 years of trial experience, is what we bring to TBI settlement negotiations.

Talk to a TBI Attorney Before You Accept

A TBI settlement is not something you can undo. If you or a family member has received a settlement offer for a traumatic brain injury, have it reviewed by an attorney who handles these cases before you sign anything.

The Leiva Law Firm offers free consultations for personal injury cases, including traumatic brain injuries. There is no cost and no obligation. Contact us at (703) 352-6400 to schedule a consultation with Manuel Leiva and get an honest assessment of whether the offer on the table reflects the full value of your claim.